Contents

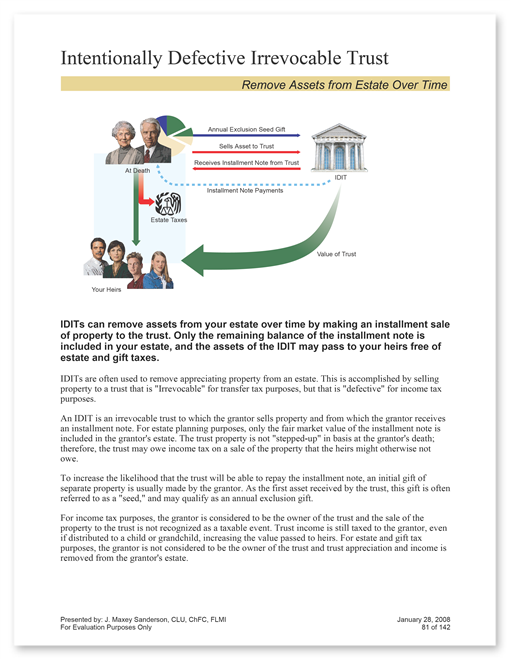

Graphic to show how this concept usually works using an installment note

Purpose

To show that instead of giving the assets to the trust, the assets are sold to the trust using an installment note. The main purpose is to have an irrevocable trust for estate tax purposes, but a defective grantor trust for income tax purposes.

Uses

Sale of assets to the trust is not a taxable event since this is a defective grantor trust. The assets and their growth are removed from the estate and replaced with the balance of the installment note.

Sales

The trust can own life insurance on the grantor to repay the installment note at death.

Transitional Uses

This method not only removes assets from the estate, but it leverages those assets through the use of the installment note.

Appeal

Individuals seeking to maximize the inheritance of their heirs and willing to take a little more risk than simply funding an ILIT